Systematic Rules for Financial Independence

Explore rules-based retirement math, track defensive model portfolios, and execute retirement simulators designed to mitigate drawdowns and sequence risk.

Automated Email Alerts & Daily Digests

Receive automated daily notifications and cadenced trend-following summaries in your inbox when defensive model portfolio signals toggle. Optimize execution without manual checking.

Tactical Model Portfolios

Analyze allocations with drawdown-protection mechanics (like Yale Endowment and Regime All-Weather) engineered to buffer down-markets.

Interactive Retirement Studio

Evaluate sequence risk, safe withdrawal limits, and custom strategy models. Backtest your configurations using clean, historical price data.

Compute historical withdrawal rates under variable asset allocation regimes.

Optimize conversions, minimize ACA healthcare costs, and plan early withdrawal bridges.

Research Guides

All Research Guides →

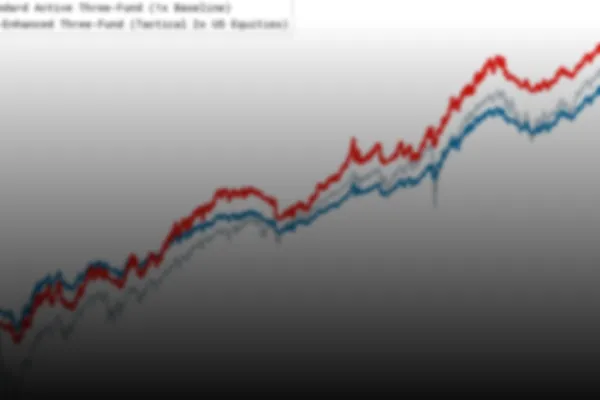

Tactical Leverage with the AlgorithmicFIRE Macro Stress Indicator

A systematic case study: boosting S&P 500 returns by adding leverage only when macro indicators indicate a low-stress market regime.

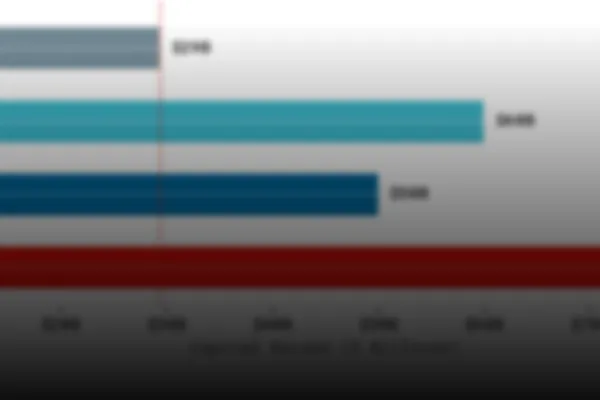

Could the Upcoming Mega IPOs Cause Substantive Price Drops Across the Public Markets?

Index funds will soon have to sell substantial holdings in order to raise the cash required to purchase shares in the upcoming IPOs of SpaceX, OpenAI, Anthropic, and others. This could cause a substantive price drop across the public markets. In this post we investigate the relative sizes of the various funds and the required cashflows to meet the demand.

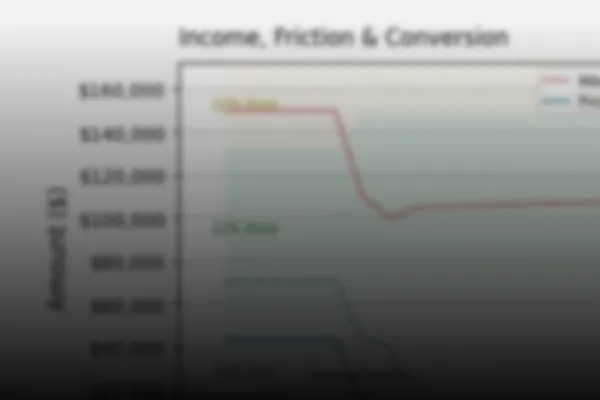

Considering retiring early, but worried about healthcare (ACA) costs?

With some financial engineering, you can reduce (and possibly eliminate) the cost of ACA coverage.

Can You Afford an Investment Advisor?

The question isn't whether you can afford an advisor, but whether the long term costs of an advisor are worth the money; which will be measured in hundreds of thousands of dollars.

Defending Your Savings Against Significant Downturns

What happens if the market doesn’t just "dip," but stays down for a decade or more? We explore strategies to safeguard your savings from prolonged stagnation.

The 4% Rule Is Dead, Here's What's Replaced It

The 4% rule, which we wrote about in our post regarding Safe Withdrawal Rate, was established back in 1994. Since then, many alternatives have been suggested. We review the major alternatives.