Investor Learning Track

A data-driven curriculum designed to build your financial independence knowledge from the ground up. Move from foundational math to advanced retirement architecture.

Curriculum Review

The AlgorithmicFIRE Curriculum Review

2026-03-20Our data-driven posts provide comprehensive resources to the math, the risks, and the strategies of Financial Independence/Retire Early (FIRE). In our Curriculum Review, we provide a summary of key posts to quick-start your journey. (Not all topics about which we have written are covered in this review.)

Saving

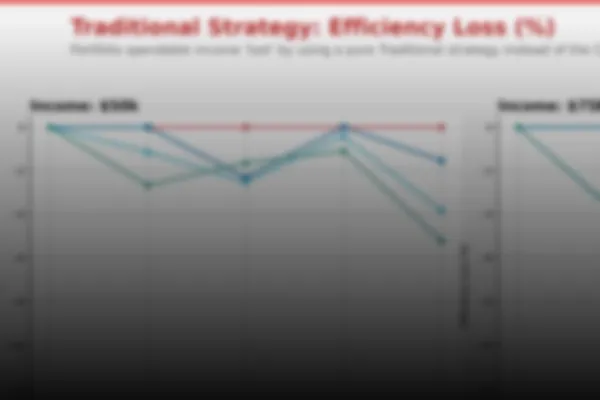

Can You Afford an Investment Advisor?

2026-01-17The question isn't whether you can afford an advisor, but whether the long term costs of an advisor are worth the money; which will be measured in hundreds of thousands of dollars.

Historical analysis shows luck plays a huge role

Except it's not. It is actually harder, unless you get lucky.

General Investing

Index funds will soon have to sell substantial holdings in order to raise the cash required to purchase shares in the upcoming IPOs of SpaceX, OpenAI, Anthropic, and others. This could cause a substantive price drop across the public markets. In this post we investigate the relative sizes of the various funds and the required cashflows to meet the demand.

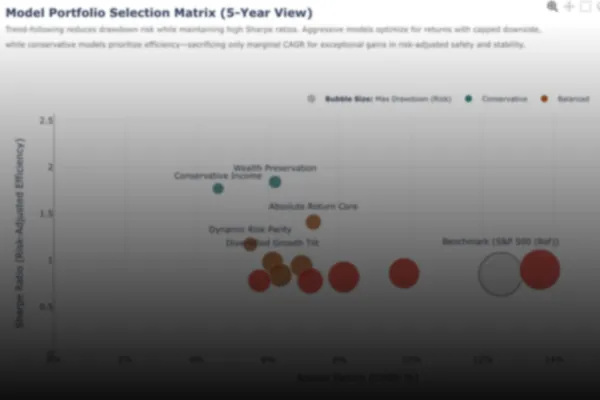

Is your portfolio achieving genuine alpha, or simply increasing volatility for marginal returns? We analyze the Selection Matrix and why vertical scaling (Efficiency) carries more weight than linear growth (CAGR).

Trend following isn't the only way to protect against downturns. We compare trend following to the "guaranteed" protection of put options, and calculate the true cost of that certainty using.

Retirement accounts are generally tax deferred, but if you have taxable accounts you should be aware of the tax implications of increased trading frequency.

What happens if the market doesn’t just "dip," but stays down for a decade or more? We explore strategies to safeguard your savings from prolonged stagnation.

When investment planning for retirement, it is important to consider all possible outcomes. We take a look at Japan in the 1990s to redefine "worst case".

Large cap indices are dominated by a few large stocks. What to know and how to get more diversified.

Understanding Sequence of Returns Risk

2025-12-05A critical risk factor that can make or break your retirement portfolio, regardless of average returns

Average Return - It’s Not What You Think

2025-12-05Compound Annual Growth Rate (CAGR) is the proper way to express investment returns over a period, not (arithmetic) average

Retirement Planning

The single most common Roth vs. Traditional question is "which is better?" We modeled the entire wealth lifecycle—from your first dollar saved to your last dollar spent—across thousands of scenarios to find out.

With some financial engineering, you can reduce (and possibly eliminate) the cost of ACA coverage.

The discussion is frequently reduced to comparing your current tax bracket to your expected tax bracket in retirement. While simple, this comparison is incomplete.

You must have a savings plan, and a withdrawal plan; either can come first. We will show you how to make both plans so you have a clear path to retirement.

The 4% rule, which we wrote about in our post regarding Safe Withdrawal Rate, was established back in 1994. Since then, many alternatives have been suggested. We review the major alternatives.

But why do they work? Why not just start with a higher withdrawal rate?

No, in fact, you are likely to leave behind substantial assets. Plan for it.

Safe Withdrawal Rate For Shorter Retirements

2025-12-05Not everyone needs a 30 year retirement. How does Safe Withdrawal Rate change for shorter retirements?

What happens if your Safe Withdrawal Rate (SWR) is too high? A look at history and some tips for recovery.

Safe Withdrawal rate (SWR) is the key to answering “Am I (financially) ready to retire?”